Part 2 of 2

This article is a continuation of “Best Practices: Helping Your Nonprofit Clients Succeed,” from CPA Publisher’s March 2026 issue. In Part 1 of this 2 part series, we examined the importance of Mission, Board Governance, Internal Controls, Form 990 compliance, and the IRS public support test.

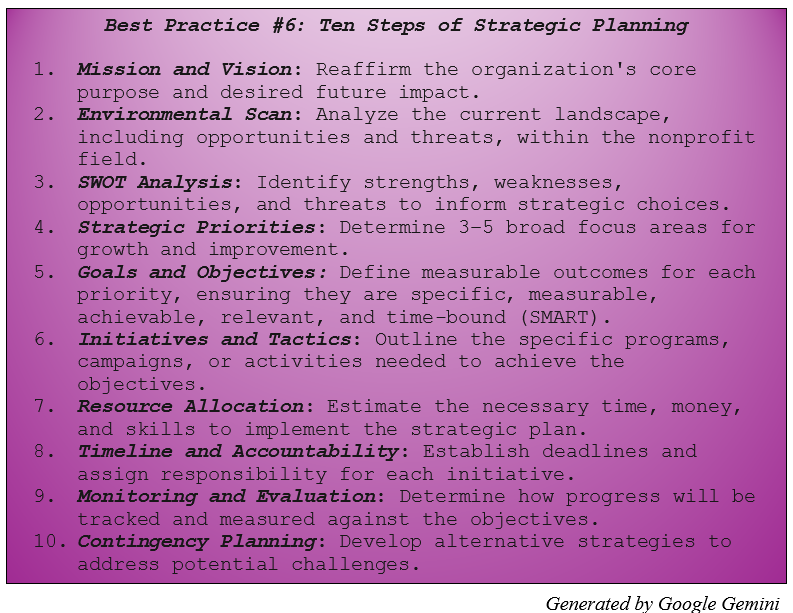

Best Practice #6: Evaluate Strategic Planning as a Governance and Risk Management Tool

A nonprofit’s strategic plan translates its mission into measurable objectives and provides the framework for decision-making, resource allocation, and performance evaluation. CPAs should review clients’ strategic plans to assess whether stated goals are clearly defined, realistic, and supported by financial and operational assumptions.

Effective strategic plans typically address key risk areas, incorporate appropriate use of technology, and establish systems for measuring and reporting outcomes, including relevant key performance indicators (KPIs). When aligned with financial planning and reporting processes, the strategic plan serves as a practical guide for prioritizing programs, allocating resources, and evaluating organizational performance.

Why does it matter?

A well-developed strategic plan supports sound governance and informed decision-making. It enables CPAs to identify potential risks, assess financial sustainability, and advise clients on aligning resources with mission-driven objectives, thereby increasing the likelihood of achieving intended outcomes while maintaining compliance and fiscal discipline.

Best Practice #7: Assess Revenue Sustainability and Donor Concentration Risk

Nonprofit clients must understand the level of recurring revenue required to sustain operations and support mission-driven activities. As an initial planning benchmark, CPAs may encourage clients to evaluate historical operating expenses and establish revenue targets that exceed annual expenses to provide adequate operating margin and cash flow stability. One commonly used planning guideline is targeting revenues of approximately 1.5 times annual operating expenses.

For example, if a nonprofit’s annual operating expenses total $100,000, targeted revenues of approximately $150,000 may provide a cushion for variability in funding, investment in programs, and unforeseen costs.

Once overall revenue targets are established, CPAs should help clients evaluate revenue composition and donor concentration. Under the Pareto Principle (the 80/20 rule), a significant portion of nonprofit revenue often comes from a relatively small percentage of donors. While major gifts play a critical role in fundraising, reliance on a limited donor base introduces financial and compliance risk that must be monitored carefully.

Why does it matter?

Donor concentration can materially affect both financial sustainability and compliance with the IRS public support test. CPAs should evaluate whether revenue dependence on major donors is consistent with public charity requirements and advise clients on diversification strategies as needed. In addition, research indicates that transparency in IRS reporting,such as filing a full Form 990 rather than Form 990-EZ,can positively influence donor confidence and revenue generation, further underscoring the importance of accurate and comprehensive reporting.

Best Practice #8: Strengthen Budgeting and Forecasting Processes

CPAs play a critical role in helping nonprofit clients develop and manage effective budgeting and forecasting processes. When aligned with the organization’s mission and strategic plan, these tools provide a structured framework for allocating resources, managing cash flow, and evaluating financial sustainability.

A budget establishes the organization’s financial plan for the upcoming period, outlining how resources are expected to be deployed across programs, supporting services, and administrative functions. A forecast, by contrast, projects future financial performance based on historical results, current trends, and known assumptions. Together, these tools enable management and the board to assess financial capacity, respond to changing conditions, and make informed decisions.

Effective budgeting and forecasting support:

- Financial resilience in the face of economic or funding fluctuations

- Increased transparency and confidence among donors, board members, and other stakeholders

- Stronger governance through ongoing financial oversight and accountability

Why does it matter?

Forward-looking financial planning is essential to sound decision-making and long-term financial health. Robust budgeting and forecasting processes help ensure that actual financial outcomes remain aligned with strategic objectives and mission priorities, reducing the risk of unintended financial or operational divergence.

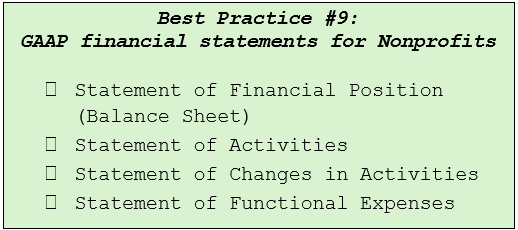

Best Practice #9: Improve Financial Statement Understanding and Analytical Use

CPAs should ensure that nonprofit clients understand the purpose, structure, and interrelationships of their financial statements. This includes explaining how information flows across statements, for example, reconciling expenses reported on the Statement of Activities with those presented on the Statement of Functional Expenses.

Through this process, CPAs can help clients evaluate expense allocation and program efficiency, including commonly referenced benchmarks such as program service spending ratios. Analyzing expense classifications and trends allows management and boards to assess operational effectiveness and identify key performance indicators (KPIs) that align with the organization’s mission and strategic objectives.

CPAs can also explain how financial statements are used externally to evaluate nonprofit performance. Donors, grantors, and oversight organizations frequently rely on financial disclosures to assess stewardship, transparency, and program impact. Rating and information organizations such as Candid, Charity Navigator, and BBB Wise Giving use publicly available financial data to inform these assessments, further elevating the importance of accurate and well-presented reporting.

Why does it matter?

A nonprofit that understands and uses its financial statements effectively is better positioned to support informed decision-making, demonstrate accountability, and enhance credibility with donors, grantors, and regulators. Clear financial reporting and analysis strengthen both internal management and the organization’s public profile.

Best Practice #10: Assess and Strengthen Technology Infrastructure

Nonprofit organizations rely on technology to manage operations, financial reporting, and donor relations effectively. CPAs should work with clients to ensure their technology supports organizational objectives, strengthens internal controls, and mitigates operational and compliance risks. Key areas include:

- Donor and contribution management: Implement systems that accurately track donations, donor information, and restricted funds to support reporting and compliance obligations.

- Online presence and reputation management: Maintain secure, professional, and informative digital platforms that communicate the organization’s mission and programs to stakeholders.

- Data security and cybersecurity: Protect sensitive information using multi-factor authentication, secure cloud services, regular backups, and other safeguards to reduce the risk of cyber threats.

- Operational efficiency and financial management: Utilize integrated tools for internal communication, program management, accounting, budgeting, and GAAP-compliant financial reporting. Technology should facilitate accurate fund accounting, reporting to grantors, and tracking of long-term program outcomes.

Why does it matter?

Robust and appropriate technology enables nonprofits to operate efficiently, maintain accurate and auditable financial records, and comply with regulatory and grantor requirements. For CPAs, assessing technology systems provides an opportunity to enhance internal controls, improve reporting accuracy, and support clients’ overall mission and strategic objectives.

Best Practice #11: Leverage the Annual Report for Accountability and Transparency

A nonprofit’s annual report is a key instrument for demonstrating impact, fiduciary responsibility, and organizational sustainability. CPAs should review clients’ annual reports to ensure that they accurately reflect mission alignment, program effectiveness, and financial stewardship.

The report serves multiple professional purposes:

- Mission and outcomes: Present the organization’s mission and highlight key programmatic achievements, using data and narrative to illustrate measurable impact.

- Stakeholder acknowledgment: Recognize donors, board members, volunteers, and other contributors, reinforcing accountability and engagement while maintaining compliance with disclosure requirements.

- Financial transparency: Include summarized financial statements and relevant key performance indicators (KPIs) to provide stakeholders with clear evidence of responsible fiscal management and program efficiency.

Why it matters:

A well-prepared annual report strengthens credibility with donors, grantors, and regulators; supports transparency; and reinforces confidence in the nonprofit’s governance and financial practices. CPAs can add value by advising on report structure, verifying accuracy, and ensuring that financial and programmatic disclosures are aligned with strategic objectives and compliance obligations.

The authors acknowledge that there are no conflicts of interest in the production of this article.

Portions of language editing were assisted using AI tools (Google Gemini, ChatGPT, OpenAI). The authors reviewed and take full responsibility for the content.

References

Better Explained. n.d. “Understanding the Pareto Principle (The 80/20 Rule)” https://betterexplained.com/articles/understanding-the-pareto-principle-the-8020-rule/#:~:text=Originally%2C%20the%20Pareto%20Principle%20referred,rough%20guide%20about%20typical%20distributions.

Byrne, Dan. 2025. “Board Diversity Leads to Better Profits.” Corporate Governance Institute. https://www.thecorporategovernanceinstitute.com/insights/news-analysis/board-diversity-leads-to-better-profits/#:~:text=Diversity%20brings%20profits,a%20priority%20for%20every%20organisation.

FreeWill. 2023. “Major Gifts: What You Need to Know for Fundraising Success.” Last modified December 11. https://www.nonprofits.freewill.com/resources/blog/major-gifts-guide-for-fundraising-success.

Give.org. 2024. “Wise Giving Wednesday: Guidelines for Good Governance.” Last modified February. https://give.org/news/guidelines-for-good-governance.

Give.org. 2026. “BBB Standards for Charity Accountability.” https://give.org/charity-landing-page/bbb-standards-for-charity-accountability.

Hsu, Wei, and Brian McAllister. 2024. “The Impact of Voluntarily Filing Form 990 on Donations, Government Grants, and Total Contributions.”Journal of Governmental & Nonprofit Accounting 13, no. 1 (May): 28–55. https://publications.aaahq.org/jogna/article/13/1/28/12566/The-Impact-of-Voluntarily-Filing-Form-990-on.

McRay, Greg. (2025). “Understanding the 501(c)(3) Public Support Test.” June 6. Foundation Group. https://www.501c3.org/understanding-the-501c3-public-support-test/#:~:text=The%20simplest%20definition%20of%20the,the%20public%20support%20test%20also. National Council of Nonprofits. n.d. “Federal Law Audit Requirements.” Last modified 2026. https://www.councilofnonprofits.org/running-nonprofit/nonprofit-audit-guidec/federal-law-audit-requirements#:~:text=Currently%2C%20as%20a%20result%20of,to%20obtain%20a%20Single%20Audit